By Charlene Crowell

The approaching spring sea- son signals not only a change in weather; but an annual surge in homebuying. Underscoring this long-standing trend is the annual April observance of Fair Housing Month.

Enacted in 1968, the Fair Housing Act banned discrimination on the basis of race, religion, and national origin in the sale or rent- al of housing by banks, insurers and real estate agents.

But fair housing for whom? While homeownership has been the primary means for most American families to build and pass on inter-generational wealth, Blacks rank last in their ability to achieve the wealth-building benefits of buying a home.

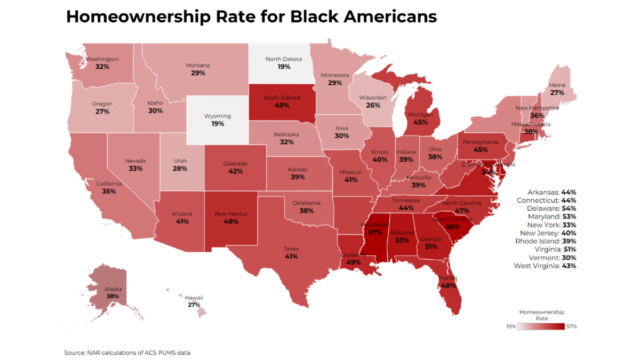

According to the National Association of Realtors’ 2024 Snap- shot of Race and Home Buying in America report, disparity be- tween Black homeownership rates and those of other racial and ethnic groups has actually grown larger since 2012. Only 44.1 percent of Blacks owned homes compared to majorities of Asian-Americans (63.3 percent), and Latinos (51.1 percent).

“The connection between homeownership rates and net worth is a critical one. Net worth, or the total assets minus house- hold liabilities, is an essential indicator of financial stability and economic well-being,” states the report.

After more than 50 years of federal laws – envisioned and enacted in hopes of helping Black America reduce lingering wealth disparities – NAR lists a litany of familiar reasons for homeownership disparities that read like a set of falling dominoes:

Median household income disparities between whites and Blacks continued to grow over the past decade. In 2012, the income gap between these two groups was $21,540. In 2022, the income gap grew to $27,840.

This gap in income is a determining factor in home affordability. In 45 of the nation’s 50 states, according to NAR, Black renters face greater affordability challenges than their white counterparts. The ability to save for a home down payment is seriously diminished when rental costs are already a financial stretch.

Another problem for would- be homeowners is that due to lower incomes and lack of savings, many Black borrowers of- ten have high debt-to-income ratios. Together, these two factors frequently lead to higher rates of mortgage application denials. In 2022, the highest mortgage denial rates occurred in three Southern states: Mississippi (34 percent), followed by Arkansas and Louisiana (each at 31percent).

A related and independent perspective from the Consumer Financial Protection Bureau (CFPB) notes yet another hurdle to homeownership: closing costs.

“While home prices and interest rates often command our attention, closing costs also con- tribute to borrowers’ monthly burdens. One measure of closing costs is total loan costs,” wrote Julie Margetta Morgan in a March CFPB blog. “Total loan costs include origination fees, appraisal and credit report fees, title insurance, discount points, and other fees increased by 21.8 percent – nearly $6,000 – from 2021 to 2022. From 2021 to 2022, median total loan costs rose sharply, increasing by 21.8 percent on home purchase loans.”

“Often, closing costs are simply rolled into the total loan amount, racking up interest for the life of the loan,” Morgan continued. “Borrowers who can’t bring cash to the table often have to pay more, through higher interest rates or mortgage insurance payments.”

But a new proposal by the Biden Administration has the potential to lessen the financial heft of these homebuying issues. In a March 12 speech before the Urban Institute, a DC-based progressive think-tank, Lael Brainard, the Biden Administration’s Economic Adviser, shared the White House plan.

“In today’s market, too many households that want to buy their first home are locked-out by high costs, while many home-owners looking to right-size their housing needs are locked-in because the rate they’d get on a new mortgage is higher than the rate on their current mortgage,” said Brainard.

Central to the administration’s plan are targeted tax credits that would enable more than 3.5 million middle-class families to purchase their first home. Eligible consumers would receive up to $10,000 in mortgage relief credit for two years – the equivalent of reducing mortgage rates by 1.5 percentage points on a median home.

“These tax credits would serve as a bridge,” explained Brainard, “as rates are projected to continue to fall with inflation and as our supply investments come online.”

Peggy Bailey, vice president for housing and income security with the Center on Budget and Policy Priorities reacted favorably.

“If policies created the inequities that we have, then we have to have policies to reverse them,” noted Bailey. “The only way to do that is to actually talk about Black People, Latinx people, Native Americans very specifically because it’s going to take very specific and targeted community investments to make those changes.”

Charlene Crowell is a senior fellow with the Center for Responsible Lending. She can be reached at Charlene.crowell@responsiblelending.org.

You must be logged in to post a comment Login